ITC – ECB October Meeting Preview: Draghi farewell, Non-event expected

Policy Announcement: Thursday Oct 24th, 12:45 BST / 07:45 ET; Press Conf: 13:30 BST / 08:30 ET

Current Rates: Deposit -0.50%, Main Refinancing 0.00%, Marginal Lending Facility 0.25%.

In Brief:

- Expectations are for no change to policy in October with zero chance of a cut priced by the market

- After the big changes in September and ongoing implementation, Oct could be a non-event

- A few areas of possible new information that analysts are watching for:

- Hints at the extent of tension within the ECB created by the Sept policy changes

- ECB expectations for tiering implementation (Oct 30th) and potential reaction function if €STR/EONIA fixes higher

- Any discussion on Issuer limits & composition of asset purchases – new QE begins on Nov 1st and likely to reach 33% limit in ~12 to 15 months under current terms

Overview:

There are no expectations of any changes to monetary policy at the October meeting since it comes just 6 weeks after the large easing package introduced in September, especially given some of the new policies introduced have yet to be fully implemented. This is the case with tiering which goes live on Oct 30th while the new QE program of €20bn per month begins on November 1st.

A lot of market participants also view this last meeting with Mario Draghi at the helm of the ECB more as a time to review his policies over his tenure and wish him goodbye. The large easing package launched in September is believed to have caused some internal turmoil within the ECB and any insights on the amount of dissent will be monitored closely. Although not likely to take place at this meeting, the market will also watch closely any comment related to the tiering implementation and the potential conditions under which the amount remunerated at 0% could change moving forward. The 6x level set in September was above the expectations of some market participants. Could this potentially be a new monetary tool by the ECB moving forward? Some market participants also believe there may be a tendency for €STR/EONIA to fix higher by a few bp on the back of the tiering implementation and analysts ask whether the ECB be ok with this increase in short term rates.

Desks are also watching for any further discussion on the QE program and Issuer/ISIN limits of 33%. This limit is expected to be reached within the next 12 to 15 months after QE goes live on 1st November. It is also the case that the actual composition of the asset buying has not been released. Although most believe the purchase mix is likely to be inline with the previous QE program, any significant changes to the composition of purchases could have an impact.

Highlights from ECB Policy Statement, Draghi’s September Introductory Statement and Q&A:

Interest Rates: “…on key ECB interest rates, we decided to lower the interest rate on the deposit facility by 10 basis points to -0.50%. The interest rate on the main refinancing operations and the rate on the marginal lending facility will remain unchanged at their current levels of 0.00% and 0.25% respectively. We now expect the key ECB interest rates to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within our projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics”.

QE (Asset Purchase Program or APP): “…the Governing Council decided to restart net purchases under its asset purchase programme (APP) at a monthly pace of €20 billion as from 1 November. We expect them to run for as long as necessary to reinforce the accommodative impact of our policy rates, and to end shortly before we start raising the key ECB interest rates.”

On reinvestment of maturing portfolio: “…to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.”

On changes to the TLTRO III: “…interest rate in each operation will now be set at the level of the average rate applied in the Eurosystem’s main refinancing operations over the life of the respective TLTRO. For banks whose eligible net lending exceeds a benchmark, the rate applied in TLTRO III operations will be lower, and can be as low as the average interest rate on the deposit facility prevailing over the life of the operation. The maturity of the operations will be extended from two to three years.”

On the introduction of tiering of deposits: “…to introduce a two-tier system for reserve remuneration in which part of banks’ holdings of excess liquidity will be exempt from the negative deposit facility rate.” More information can be found using the following link: ECB introduces two-tier system for remunerating excess liquidity holdings

On risks on medium term inflation outlook (statement): “Today’s decisions were taken in response to the continued shortfall of inflation with respect to our aim. In fact, incoming information since the last Governing Council meeting indicates a more protracted weakness of the euro area economy, the persistence of prominent downside risks and muted inflationary pressures. This is reflected in the new staff projections, which show a further downgrade of the inflation outlook”

Street Views:

-Barclays: Draghi will avoid attempting to guide the market in either direction and instead focus on handing over the baton to Lagarde. After the package announced in Sept, no new policy announcement is forthcoming.

-Commerzbank: The last Draghi meeting this week will be one of the most boring since he took over the reins of the council. The meeting will mainly be about celebrating his legacy of saving the Euro and avoiding any mention of any disagreement within the GC

-Danske: Expect no changes in policy with market reaction to the meeting likely muted

-ING: the meeting will be a non-event for policy. Expect Draghi to reconfirm the economic assessment, reiterate the Sept decision, downplay any internal divergence and provide no hints of additional measures

-Lloyds: believe the meeting should be a non-event with most of the focus being on Draghi’s legacy.

-MS: Draghi likely to reiterate that the package introduced in Sept was appropriate and now it is the turn of fiscal policy to take over. Still foresee a 10bp Depo cut at the March 2020 meeting.

-Natwest: Draghi’s last ECB meeting will be a quiet one. See no change in policy for the remainder of 2019. NWM push back their call for another rate cut until March 2020. Expect Draghi to push for fiscal policy to support demand

-Nordea: This meeting will focus more around Draghi’s legacy at the ECB. Some areas of potential interest incl the distribution of QE assets purchases, hints regarding the ISIN 33% limit and potential increase in €STR rate due to tiering beginning on Oct 30th

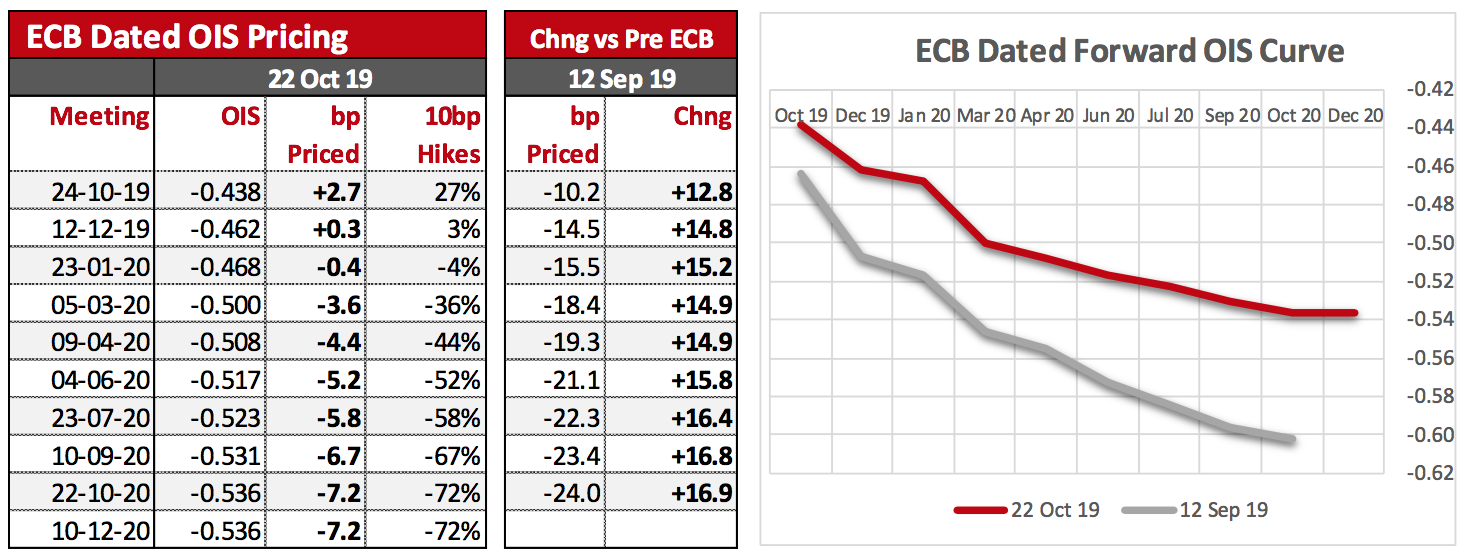

What’s Priced In?

OIS markets presently price in a 0% probability of a 10bp rate cut at the October meeting with a 50% probability of a 10bp cut by June 2020. Of special interest is the potential increase in fixing level associated with the implementation of tiering which begins on the 30th of October.

Some Recent comment from GC members:

Oct 10th – Rehn (Very Dovish): Recent split in central bank decision-making has some effect on policy; ECB still has some time before QE limits become a problem

Oct 17th – Visco (Very Dovish): I did not agree on all pieces of the Sept package; Don’t think negative rate environment is normal; must be mindful of side effects of negative rates; Starting to see spill over to service sector; it would’ve been better to name dissenters in ECB account

Oct 16th – Lane (Dovish): EZ facing a more extended slowdown than previously expected; we’re prepared to be patient in raising inflation back to target, but inflation momentum has to be there; we can go “quite a long time” buying at the current limits; APP limits were put there for a “good reason”

Oct 8th – Hernández de Cos (Dovish): Evidence suggests we haven’t yet reached the reversal rate

Sept 24th – Kažimír (Dovish): Sep policy decision was the right one, the ECB moved ahead of the curve; opponents of QE held their views for a long time

Sept 16th – Stournaras (Dovish): Strong case for Lagarde to keep up stimulus; there’s been insufficient contribution from fiscal policy

Sept 23rd – Lagarde (Dovish): Threat against trade is the biggest hurdle for global economy; US econ is in a very good place; European fin situation has changed ‘massively’ since crisis; fin risks will be unanticipated; Europe will be in good shape if there’s joint efforts to steer the econ

Oct 18th – Draghi (Dovish): Governing Council continues to stand ready to adjust all of its instruments as appropriate; Effectiveness of Mon Pol can and should be enhanced by other policies Resilience of EA banking sector remained solid; there are mild signs of overstretched valuations in the EA in some riskier segments of fin mkts

Oct 14th – de Guindos (Dovish): Latest development regarding US/China trade deal are good news; low profitability among banks in the EZ is among main vulnerabilities; unavoidable consolidation of by banks in EZ is hampered by low valuation of lenders; does not see a EZ recession but a long period of low economic growth

Sept 22nd – Vasle (Dovish): Global economic conditions are very complicated, ECB action will probably be necessary in the coming months, quarters & years

Sept 19th – Herodotou (Dovish): “The current economic conjuncture in the euro area, the slowing inflation and the various geopolitical uncertainties advocate the use of pre-emptive measures,”; “The measures send a clear signal and response to the persistent shortfalls and downward outlook of inflation. The measures decided mitigate the risk of running behind events.”

Sept 19th – Cœuré (Hawk): If we embarked on QE forever it would remove the need for market discipline but there is no sign of that; been venturing close to the line between monetary and fiscal policy but there are safeguards; no risk sharing clauses of PSPP among safeguards

Oct 21st – Villeroy (Hawk): Fiscal policy must help mon pol support the global economy; expansionary mon pol must remain active amid low inflation, but they aren’t sufficient; all available instruments need to be mobilized including fiscal policy as a complement to mon pol

Sept 19th – Lautenschläger (Hawk): See global growth amid trade & political risks; Spanish & Dutch economies seen resilient, German economy is weakening from trade tensions; overall EZ domestic demand has been resilient & financial conditions are excellent; central banks shouldn’t be the only game in town, other stakeholders have to step up

Oct 10th – Holzmann (Hawk): ECB should lower inflation target in upcoming policy review, would support 1.5% or even lower; pension funds, insurers can’t adjust to negative rates; in the long run, negative rates are not sustainable; indications that euro zone economic improvement is on its way; making ECB voting record public is way to improve transparency and accountability

Sept 23rd – Knot (Very Hawk): Not in full agreement with ECB stimulus; open ended QE was a disproportionate measure; important to keep discussion open in ECB board; need to explore bandwidth on inflation target; don’t know if savers will pull cash form banks if we see negative interest rates; looser fiscal policy makes send for Europe but not for the Dutch economy; European economy growing at full capacity; confident inflation will return to roughly 2% over time; no need for law against neg rates; European budget rules should focus more on national debt, less on deficits

Oct 1st – Weidmann (Very Hawk): Imperative that far-reaching measures such as government bond purchases lead to intensive discussion; he hopes that decisions will not lead to app restrictions being called into question

Analyst: Robin Belec