US Election Survey Results – Investors warming to a blue tsunami

We recently surveyed clients on expectations around the upcoming US election. This marked the second iteration of our US election survey, with the first having been conducted in early August. The survey was open from 8-12 October and we received more than 50 responses, closely matching the number of responses from our first election survey. Respondents included both US and globally-based investors, surveyed via our distribution channels. The following represent the key findings from our survey:

- Expectations on a Biden victory are increasingly cemented

- The election has factored more heavily in price action

- Expectations are for results to emerge within one-week of polls closing

- The election is not expected to stand in the way of the broader USD downtrend

- A Biden victory is seen as increasingly risk positive, suggesting market response hinges on phase 4 stimulus prospects

- Phase 4 stimulus is now expected post inauguration

Expectations on a Biden victory are increasingly cemented and the Senate is expected to turn blue – Since we first surveyed investors in early August, expectations for former VP Biden to take the Presidency have grown. Nearly 90% of survey respondents expect Biden to win, compared to 73% in the first iteration of our US election survey. If anything this points to somewhat stronger expectations for a Biden victory among survey respondents than might be anticipated on the basis of polling averages/popular election models, which point to a touch lower probability for a Biden win. It follows then that fewer survey respondents believe polling averages overstate the likelihood for Biden to secure victory than was the case with our previous survey. Survey respondents increasingly expect Democrats to take control of the Senate. 74% of survey respondents look for Democrats to take control compared to only 57% at the time of our last survey.

The election has factored more heavily in price action – The number of survey respondents who believe that the election has been a major factor in FX and asset market price action has jumped sharply over the past two months. 51% of survey respondents now believe the election has been a major factor, compared to only about 16% in the previous iteration of our survey. 41% if survey respondents believe the election has been a minor factor, while the percentage of respondents who believe the election has not factored at all, has been more than halved to 7.8%. While this implies that investors believe election risks should at least be partly discounted at present, a majority still look for some risk reduction to feature ahead of the election itself. About 63% of survey respondents look for risk reduction compared to 81% at the time of our last survey.

Expectations are for results to emerge within one week of polls closing – While the percentage of survey respondents looking for results to be clear on election night has declined slightly over time to about 21.5%, the overwhelming bulk still expect results within one-week. Less than 16% of survey respondents expect the ‘tally’ to take longer than a week. It is not surprising that investors would be marginally more confident that a contested election result will not be seen in the wake of the perceived widening of Biden’s advantage over President Trump coming into the vote and it is possible that this has been a factor lending support to risk appetite. Of course, this leaves open the door to a risk-negative shock to markets should a drawn out process of determining a winner be seen similar to Florida recount in 2000.

The clear bias remains that a Florida-redux scenario would be risk negative. Nearly 90% of survey respondents expect SPX to fall if it takes longer than one week to arrive at clear results, up from about 79% of survey respondents in August. 92% of survey respondents look for non-USD safe-havens to outperform in this scenario, while there is less consensus on USD direction itself. 45% of survey respondents expect USD to rise, 43% expect USD to fall and about 12% expect the dollar to be roughly unchanged. This marks a drop in the percentage of respondents looking for USD to fall, which may reflect the belief that positioning has shifted in favor of USD shorts, so risk reduction could lend support.

The election is still not expected to stand in the way of the broader USD downtrend – About 53% of survey respondents expect USD to decline in the three-months following a Trump victory and 65% of survey respondents expect a lower USD three-months after a Biden win. This compares to about 31% expecting USD to be higher on a Trump victory and 16% on a Biden victory, with the remainder looking for USD to be roughly unchanged. The conclusion is that irrespective of the victor of the election, there is expectation for an extension of the USD downtrend in the medium term. Previous election cycles have most often not been associated with shifts in the broader trend in FX markets.

There is less consensus around the ‘short-term’ impact. A majority of investors expect USD to be unchanged or higher within one-week on a Trump victory, while a majority expect USD to be unchanged or lower on a Biden victory.

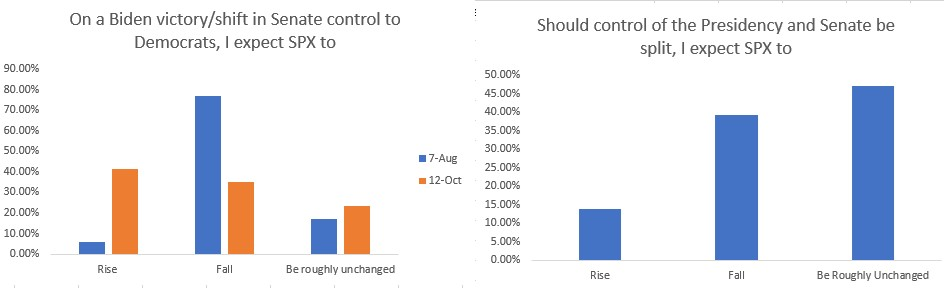

A Biden victory is seen as increasingly risk positive, suggesting market response hinges on phase 4 prospects – There has been a sharp shift in expectations for SPX response to a Biden victory. More than 37% of survey respondents expect a Biden victory to see a rise in SPX, compared to only 13% at the beginning of August. Only 27% see SPX declining on a Biden victory compared to nearly 64% at the beginning of August. Expectations that a Trump victory would see higher equities are unchanged. This looks consistent with expectations that there is reduced risk for a contested result and that a blue tsunami, in which Democrats take the Presidency and the Senate, could be associated with a push for more pronounced fiscal stimulus. Investors appear less concerned with potential rises in taxes and tighter regulation under a Biden presidency. Note, the overwhelming likelihood is for Democrats to retain and consolidate control of the House.

Indeed, when queried on this specific scenario, the largest set of survey respondents look for SPX to rise, contrasting our earlier survey results. SPX performance on a split Presidency and Senate is expected to suffer. Less than 14% of survey respondents expect SPX to rise in this scenario. This supports the view that investors are increasingly focused on prospects for passage of phase 4 stimulus as the key determinant of market price action in response to the election. A Biden victory is seen as more positive for yields, with 69% of survey respondents looking for higher 10yr yields, compared to only 33% should Trump prove victorious.

Unsurprisingly, investors see a split Presidency/Senate as favoring outperformance from non-USD safe-havens, albeit by a much smaller margin than was the case in August. 41% of survey respondents expect non-USD safe-havens to outperform, 37% expect them to underperform, while 22% look for roughly even performance with risk currencies. The largest segment of survey respondents expect USD to be roughly unchanged on split control of the Presidency/Senate, perhaps reflecting expectations for push and pull between selling against safe-havens and buying against risky currencies. Should the blue tsunami play out, the implications appear to be more clear cut for USD weakening. The scenario in which President Trump wins another four years but Democrats take control of the Senate looks less likely to occur.

Phase 4 stimulus is now expected post inauguration – About 75% of survey respondents look for phase 4 stimulus to be signed into law after the new Congress/President is sworn in in late January. Few expect a full package before the election, although a the largest segment of survey respondents believes standalone measures could be enacted in the next few weeks. Less than 2% look for a full package to be passed pre-election, with a significant minority looking for stimulus to come in a lame duck session despite the challenging politics that might prevent action. About 22% of survey respondents look for this eventuality. Less than 2% expect no stimulus to be passed at any point in the months ahead. While this looks consistent with most of the expectation for immediate stimulus having been removed from the market, there could yet be some scope for further paring. We would also note that with few investors looking for standalone stimulus measures during the lame duck session (only about 22% of respondents), this may understate the risk for targeted measures to be attached to the mid-December spending bill, which might prove risk positive.