ITC – BoE November Preview: With another Brexit Delay & a Dec 12th election, more wait and see

Thursday, November 7th: Policy Decision & MPR (new name for QIR) release: 12:00 GMT; Press conference 12:30 GMT

Current Policy: Bank Rate: 0.75%; Asset Purchase Programme: £435bn; Corp Bond Purchases: up to £10bn

In Brief:

• Analysts expect no change in monetary policy including rates & QE

• MPC likely to vote 9-0 for keeping all policy unchanged

• Most analysts believe everyone on the MPC is firmly in ‘wait and see’ mode due to uncertainty created by the extension of the Brexit deadline and the upcoming Dec 12th general election.

• Markets pricing no move in November and only nearly 50% of a 25bp cut by June 2020.

• Monetary Policy Report (MPR) released at this meeting. Focus will be on BoE’s estimates for:

o Inflation forecast: In August, forecast in 2yrs was 2.23% & 3 years at 2.37%.

o GDP growth: In August, forecast in 2yrs was 2.42% & 3 years at 2.50% (with rates unchanged at 0.75%)

o Unemployment rate: In August, forecast in 2yrs was 3.70% & 3 years at 3.30% (with rates unchanged at 0.75%)

• Some analysts believe the MPR may slightly revise inflation lower for the 2 year and 3 year horizon mainly due to the recent rebound of GBP. (NWM forecast 2y inflation at 2.13% and 3y at 2.22%)

Overview:

In similar fashion to the September meeting, the MPC will meet this week against the backdrop of mixed but steady economic data, tight labour markets, Brexit-related uncertainty and now a new election scheduled for Dec 12th. Against this uncertain backdrop, analysts unanimously expect no change in the current bank rate, with everyone calling for a 9-0 vote. All QE parameters (Asset Purchase Programme and Corporate Bond Purchase Programme) are also expected to remain unchanged.

With the launch of new elections for December 12th plus the extension once again of the Brexit deadline, political/economic uncertainty has continued to push to the future any change in monetary policy. Interestingly, this particular election will also include a Brexit theme with different parties pushing different views on how to solve the Brexit dilemma on top of their own economic agendas. The Conservative Party want to push through their negotiated version of the Brexit deal, Labour wants a second referendum on Brexit, the Liberal Democrats what to pull article 50 and the Brexit party simply wants a Hard Brexit period. Meanwhile the Scottish Nationalist Party seek to break up the United Kingdom via a second Separatist referendum, assuming Brexit goes through after January 31 2020. Although polls suggest the Conservatives have an early lead, the 2017 election has reduced the confidence in the potential outcome. Interestingly voters at the election will need to make a decision on their own priorities: their own desire with regards to a Brexit resolution or voting for the party representing their own views on economic agendas. The result of this combined election/referendum having the potential to create some very surprising results. Many parties have also promised the loosening of fiscal policies if they win to increase the support of potential voters.

With high UK political uncertainty, a pushed back Brexit deadline, a global economy weakening on trade conflict, a low UK unemployment rate (3.9%), solid average earnings (3.8%) but tepid headline inflation (at 1.7%); it is difficult to see the MPC making any changes to monetary policy or even attempting to guide markets one way or the other. The likely outcome is the MPC simply stresses that they are prepared to move in either direction depending on the outcome of Brexit. Potentially they will reiterate that the UK economy is relatively strong, and assuming a ‘soft’ Brexit is implemented, project likely small increases in rates over the next few years. The combination of a strengthening GBP vs. other major currencies is also seen adding another dimension to the jigsaw puzzle, as are tail risks tied to second referendums on Brexit and Scottish independence.

The Bank of England also announced on October 31st, that the Quarterly Inflation Report would undergo some changes to its structure/content and they had therefore decided to rename the report the Monetary Policy Report. The new report giving greater prominence to their analysis of the economic outlook plus introduction of a new ‘In Focus’ section to describe issues that have received particular attention in the latest forecast thereby making the report more thematic.

What’s Priced In:

Although at the beginning of October the market saw an increased probability of a Hard Brexit, Boris Johnson’s ability to negotiatie a new deal with Europe quickly saw the hard Brexit probability reduced. The market is now pricing only a 25% probability of a 25bp rate cut by March 2020 and just shy of 50% probability by June of next year.

Street Views:

-Citi: MPC will unanimously vote to keep Bark Rate unchanged at 0.75%. MPC doves will point to weak economic confidence while hawks to robust wage growth. If voters decisively back the Conservatives’ Brexit deal or a ‘Remain alliance’ and a second referendum plus the winners execute fiscal easing, hikes could follow next year.

-GS: No change expected at this November meeting due once again a delay on Brexit and the upcoming December election. They view the UK economy to be relatively sound with labour market close to full capacity and core inflation to settle around the 2% level and therefore prevents the MPC from initiating a cut in rates at this juncture Nevertheless if the election results in once again a poorly functioning parliament with the potential for another Brexit delay past January, could result in a rate cut before Governor Carney steps down.

-Lloyds: Expect unch policy with almost certain of unanimous vote. BoE will acknowledge the weaker external environment and ongoing political uncertainty but nevertheless the bank will reiterate that assuming a smooth and orderly Brexit, they expect modest increases in the Bank Rate although with increasing conditionality.

-NWM: BoE highly unlikely to announce any change in monetary policy in November. The combination of an imminent general election, some progress towards a Brexit deal, upwardly revised Q3 GDP and a more expansionary fiscal policy will likely leave the BoE with a slightly hawkish tilt. Neverhteless NWM is still forecasting a 25bp rate cut in May 202o with the risk of a second rate cut of 25bp in Q3 2020.

-TD: BoE to keep policy rates unchanged but move further away from its long-standing hiking bias, and the macro forecasts more likely to signal that the market pricing of the probability of a rate cut no longer so far fetched as the MPC moves to a more balanced view.

September Decision Statement and Minutes:

The MPC’s September decision statement and Minutes left all policy unchanged with a unanimous vote and showed that the MPC feels there is increasd uncertainty on how the economy will develop due to Brexit.

“entrenched Brexit uncertainties and slower global growth have led to the re-emergence of a margin of excess supply. Increased uncertainty about the nature of EU withdrawal means that the economy could follow a wide range of paths over coming years. The appropriate response of monetary policy will depend on the balance of the effects of Brexit on demand, supply and the sterling exchange rate.”

In the event of a smooth Brexit, the MPC still believes increased in rates at a gradual pace would likely be needed.

“In the event of greater clarity that the economy is on a path to a smooth Brexit, and assuming some recovery in global growth, a significant margin of excess demand is likely to build in the medium term. Were that to occur, the Committee judges that increases in interest rates, at a gradual pace and to a limited extent, would be appropriate to return inflation sustainably to the 2% target.”

August QIR Forecasts Summary:

Source: Inflation Report, BoE – forecasts from February QIR are in the brackets

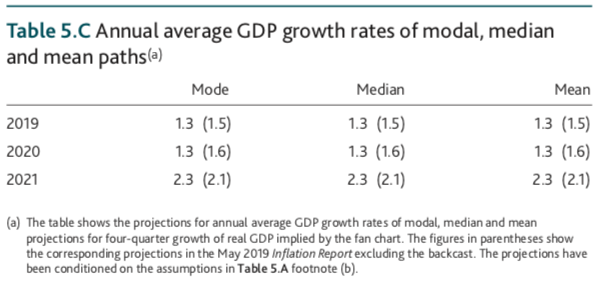

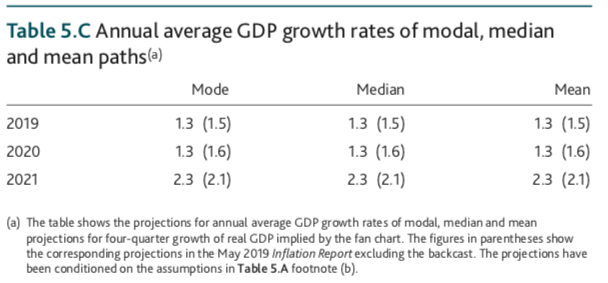

Annual Average GDP growth rate projection:

August QIR had seen a significant revision lower in GDP relative to May QIR numbers. Some expect that 3rd Quarter GDP should see a rebound after the disappointing number in Q2 but it is uncertain that this will be enough to revise GDP projections upward.

Annual Average CPI Inflation projection:

Looking at the CPI inflation projections based on market rates, the August CPI inflation projections for inflation 2yrs was 2.23% & 3 years at 2.37%. The November QIR report will be scrutinized closely to see if there are any changes to these projections. With the GBP having strengthened in October, expectations are for the inflation forecast to be revised lower.

Recent BoE Speakers

October 14th – Cunliffe (Dovish): These ‘low for long’ rates pose these challenges: pressure on the resilience of the financial sector; increased leverage among households and businesses risk of more severe economic downturns; a great deal of careful deliberation needed before changing monetary and fiscal framework due to structurally low interest rates; a world in which downturns are more significant because of less effective demand management would be a big challenge for financial stability; we need active and powerful macro-prudential institutions and policy, counter-cyclical capital buffer may need to be made more powerful if interest rates low for longer; low market rates prob reflect over pessimism about L/T growth with increased pressure on banks to hunt for yield & take more risk; mon pol not powerless but expect more tools will be needed to stimulate demand in downturns ; too early to say we need more coordination between mon & fiscal pol

October 15th – Vlieghe (Dovish): Stimulus needed if Brexit uncertainty becomes entrenched; Slack in the UK is increasing again; global outlook has deteriorated since July; sees risk of monetary policy running out of ammunition; scenario of entrenched Brexit uncertainty is likely to require stimulus; BOE should consider buying private sector assets in the future, if a particular asset class is under stress; prob been working too long with the assumption that Brexit uncertainly will soon reduce

October 13th – Ramsden (Neutral): Smooth Brexit would put rate hikes on the table; BoE will watch FX mkt’s on Sunday after the Brexit vote; limited & gradual is a reasonable qualitative framing of rate hike stance

October 28th – Tenreyro (Neutral): Simple macroeconomic estimates of effect of trade barriers probably underestimate effect of tariffs; exchange rates continue to have important effects on export volumes

September 27th – Saunders (Neutral): BoE’s next move could ‘quite plausibly’ be a cut even if no-deal Brexit is avoided; deferring monetary policy changes until after Brexit could lead to inappropriate policy; rates could go either way after Brexit; Brexit uncertainties are a slow puncture for the UK economy; floor for UK rates is zero or marginally positive; not a fan of negative interest rates; negative rates lead to a weaker banking system and financial instability; if there was no Brexit uncertainty the UK economy would be in its best position for decades; below potential growth is enough to justify a rate cut, do not need a further slowdown

October 18th – Carney (Neutral): Cannot pre commit to rate hikes if Brexit deal passes; Have many other tools beyond Mon-Pol

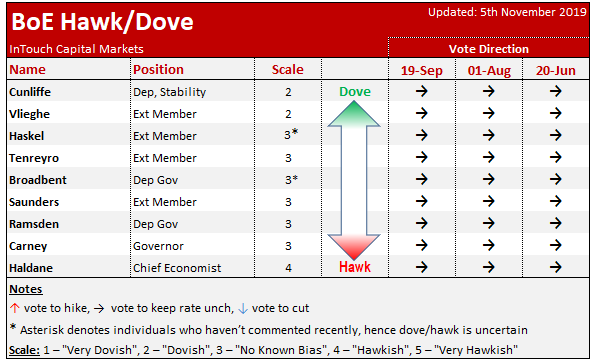

ITC’s BoE Hawk-Dove & Recent Voting History:

BoE Update – 5th November. What’s Changed?

We moved Ramsden a couple of positions lower, but still in the neutral side of the scale, after highlighting that smooth Brexit would put rate hikes on the table. Otherwise, it’s probably fair to say there is less dispersion of views across the MPC lately with all members effectively in wait and see mode for any policy response required after hard/soft/delayed/no Brexit. At the last meeting, the MPC unanimously voted to maintain rates at 0.75%.