ITC – Italian 3y and 7y BTP Auction Preview

Italian Auction:

On Thursday at 10:00 GMT, Italy will auction BTPs: €1.75 – 2.25bn 3y 0.05% Jan23 (~RX 4k futs) and €2.25 – 2.75bn 7y BTP 0.85% Jan27 (~RX 12k futs)

Overview:

As a result of the €9bn 15Y BTP syndication, the Italian Treasury has ducked any longer dated issuance at this auction and so the duration being sold to the market is modest. These auctions should get good domestic sponsorship and go fairly well.

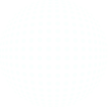

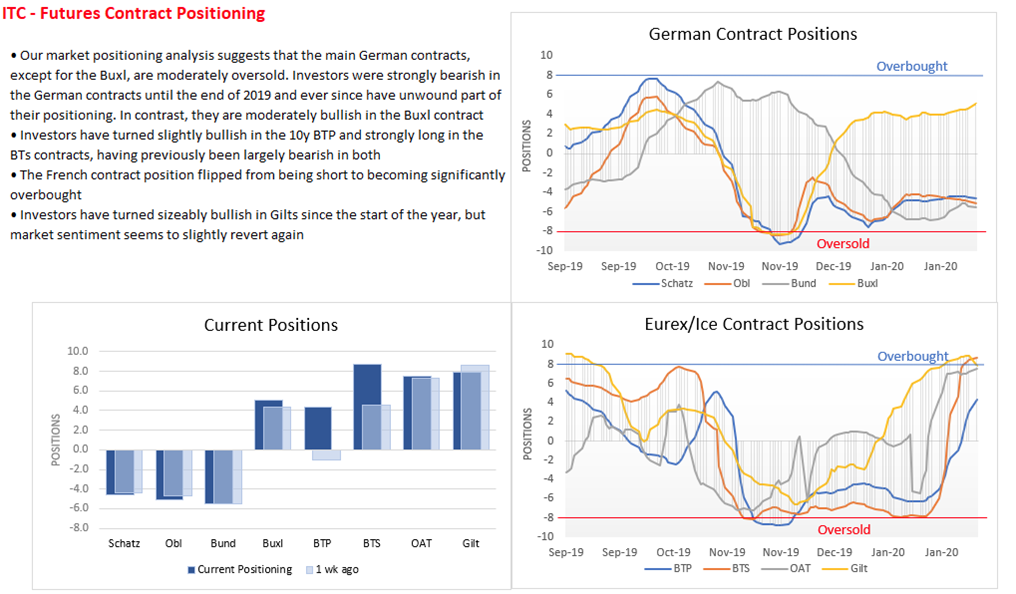

The record €50bn+ orders for the 15y suggests a strong demand for BTPs but we’ve written enough auction previews to know that large orders at a syndication do not correlate with successful subsequent auctions. Italy sees a lot of redemptions/coupons around this time of year, with a slug just paid on 1 Feb and another €33bn approaching on 2 March. ITC European market futures positioning calculations suggests that the market is long BTPs and many banks continue to write about the benefits of BTPs given a calmer political backdrop. Italian banks tend to sell BTPs heavily in December and then buy back in January and to some extent February; the 3y and 7y BTPs would be maturities on their shopping lists.

Italian banks have shown a strong seasonal pattern in their purchases of Italian bonds. They generally sell in December, probably to reduce their balance sheets but then buy back in the first months of the following year. This might be partly due to an expansion in the size of the BTP market, but there is still likely to be good buying in February.

Bank portfolios tend to cluster around the sub 10y sections of the yields curve and so if seasonal patterns remain the same (and there was a €10.6bn sale of Italian bonds in Dec-2019 and €5.6bn in Nov-19, although introduction of ECB tiering might complicate the pattern), then this auction should be reasonably well-sponsored by the Italian banks.

On the negative side, analysis of the futures market suggests that January has seen a large build on net longer positions in the front (BTS in particular) and back end of the yield curve.

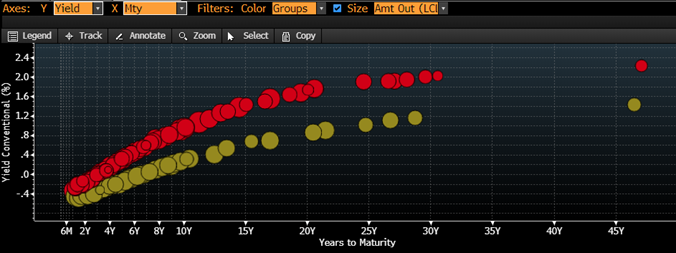

In terms of potential along the yield curve, if the Italian credit continues to improve then, it would be natural to expect that the Italian curve shape would gradually converge upon that of the next best credit – Spain. Generally, the lower the credit rating, the steeper the yield curves in the EGB space and the Italian curve is steeper than Spain’s (see chart below). However, this is generally only true up to the 20y section of the Italian curve (perhaps helping the 15y received strong orders). However, the steepest place of divergence between Italian and Spanish curves is approximately between the 3y and 8y section. In short, this part of the curve has greatest flattening potential relative to other EGB curves. BTP bulls might start creeping into bonds such as the BTP 0.85% Jan-27 that is on sale Thursday.

Italian (red) and Spanish (green) yield curves

As the Bund-BTP spread narrows, the market will be more apt to iron out relative slope differences between the yield curves. Currently, much of the semi-core sub-10y is almost indistinguishable.

10y Bund-BTP 10y spread

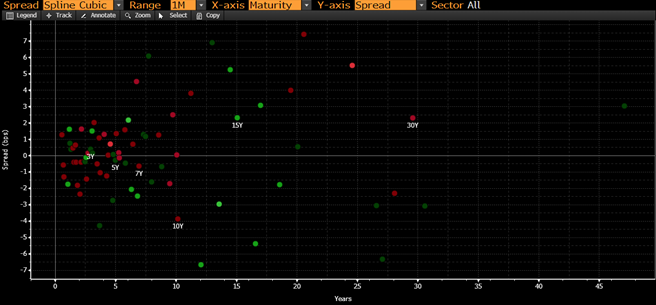

In terms of micro-RV, both of the bonds on sale trade very close to the cubic spline curve and in line with the Z-spreads of other bonds in their sectors.

Spreads to the cubic spline curve (the two auction securities are labelled 3y and 7y)

Italian cash flow is negative this week and equal to the conventional issuance. Near-term cash flow (within next four weeks) turns highly positive at €19.29bn, with €32.79bn coupons and redemptions being paid on 2nd Mar and offsetting the expected conventional issuance of €13.50bn

History:

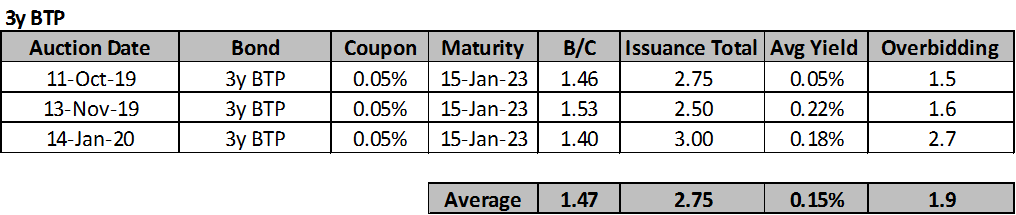

- The last 3y BTP was tapped Jan 14 with a cover ratio of 1.4x (vs. the average of 1.47x seen in the previous 3 auctions), with an average yield of 0.18% (vs. the average of 0.15% seen in the previous 3 auctions) and overbidding of 2.7cts (vs. the average of 1.93cts seen in the previous 3 auctions)

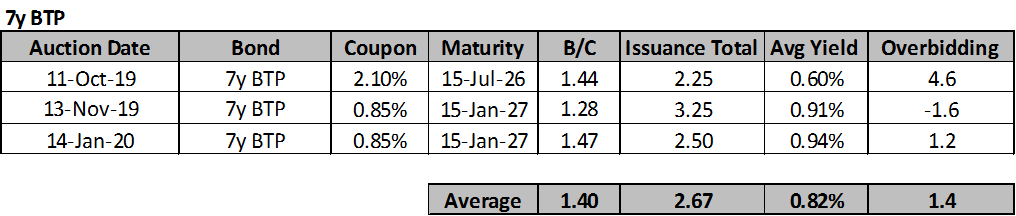

- The last 7y BTP was tapped Jan 14 with a cover ratio of 1.47x (vs. the average of 1.4x seen in the previous 3 auctions), with an average yield of 0.94% (vs. the average of 0.82% seen in the previous 3 auctions) and overbidding of 1.2cts (vs. the average of 1.4cts seen in the previous 3 auctions)

Previous auction stats: